Budgeting & saving

Young and broke? There’s another way

19 March 2018

Share

Subscribe to Money & Life

Budgeting & saving

19 March 2018

Share

When you’re young it can seem like you’ll always be living from paycheck to paycheck with nothing left for the good things in life. According to guest contributor, James Trethewie Financial Planner AFP®, making a few changes to your money habits and attitude can make all the difference to your lifestyle, now and in the future.

If you’re not great at sticking to a budget, you’re not alone. The average level of household debt has more than doubled in the last 12 years[1] and 55% of Australians owe money on their credit card[2]. But if you accept this as the norm and carry on spending as if your debts don’t matter, you’re storing up trouble. When you have something important to spend on in the future – like your first property or getting married – those debts are going to really hold you back. So it’s really important to tackle debts now by figuring out what you owe and committing to a schedule for paying them off.

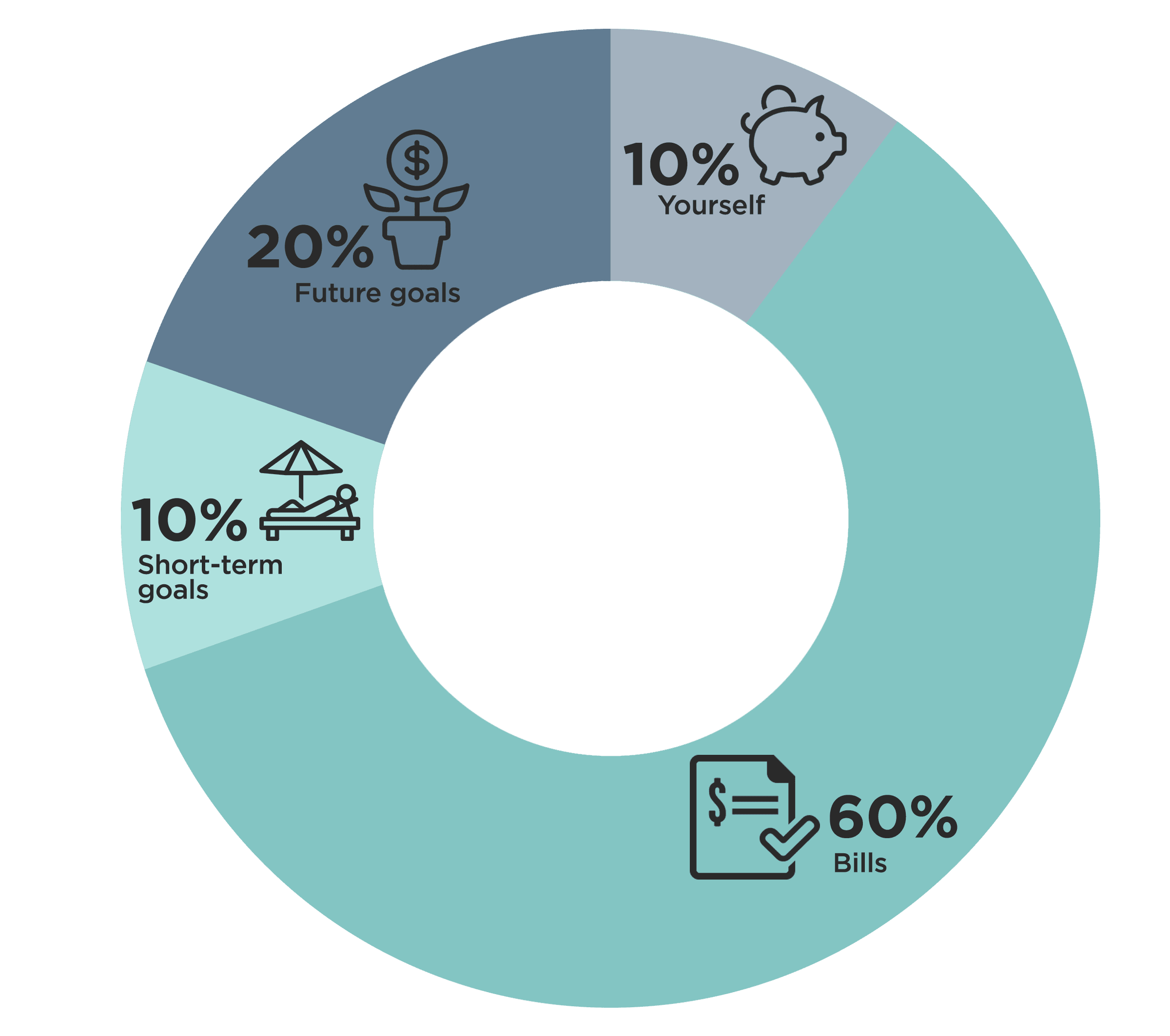

Budgets are much harder to stick to when all your spending comes from the same pot of money. If this is the way you operate – and most of us do – it takes lots of discipline stay on track with spending and saving. You can make the whole process much easier by having four separate accounts for your income, divided up roughly like this:

Make sure the accounts for saving money don’t come with a card to make it easier to keep from spending it when you’re tempted. And remember that bills should include all loan repayments as well as other regular outgoings like rent, groceries and travel. These percentages are only recommendations and you may need to tweak yours to match current commitments.

One of the more sizeable chunks on the cash flow chart is the money you channel towards long-term savings. Not only is this the money you’ll be glad to have when planning to buy a home or start a family, it also doubles as your emergency cash stash for big unexpected bills. Without this money up your sleeve, paying to have your car fixed or to replace your fridge when it bites the dust will likely go on your credit card. And that just delays the process of getting yourself debt-free.

When you’re young and especially when you have debts to pay off, getting into a better situation with money can seem impossible. House prices are going up and having to choose between saving and giving up smashed avo on toast, let alone cancelling your plans to travel and see the world, feels really unfair. But even a tiny amount of money – $10 or $20 a week – is going to have a big impact if you start saving right now.

The magic of compound interest is that it only takes a small amount, saved regularly over your lifetime to make a big impact on your wealth. Check out the ASIC compound interest calculator and the figures speak for themselves. It’s not a way to turn your dollars into millions overnight but it’ll move you closer every day to where you want to be.

A few words of wisdom about following fads that could make you rich overnight. You’re probably hearing all sorts of stories in the media about cryptocurrency and people who’ve made $1000 into a $1 million by leaping on and off the Bitcoin bandwagon at just the right time. But Bitcoin – and lots of other get rich quick solutions – is no more likely to make you rich than heading to the casino or racecourse with your all your earnings for the week. Trying to make your fortune this way can be a bit of fun, but only if it’s money you can afford to lose altogether.

Looking for more advice to get you on top of your finances? Learn about 5 financial hacks to set you up for life in your 20s and 30s and discover more tips from James for managing money in your 20s, 30s and 40s.

[1] News.com.au, ABS research reveals household debt has doubled over 12 years, Sophie Ellsworth, 13 September 2017, “The Australian Bureau of Statistics Household Income, Wealth and Expenditure Survey has found the average amount of debt has almost doubled in the past 12 years — from $94,100 in 2003-04 to $168,600 in 2015-16.” http://www.news.com.au/finance/money/budgeting/abs-research-reveals-household-debt-has-doubled-over-12-years/news-story/43f29dc69102cf86ef2184bbdf78b244

[2] News.com.au, ABS research reveals household debt has doubled over 12 years, Sophie Ellsworth, 13 September 2017, “plastic debt was held by 55 per cent of the population” http://www.news.com.au/finance/money/budgeting/abs-research-reveals-household-debt-has-doubled-over-12-years/news-story/43f29dc69102cf86ef2184bbdf78b244