Renewed focus on personal investment [CPD Quiz]

09 March 2018

Share

09 March 2018

Share

This article is worth

FPA members can earn CPD hours by reading some of the articles on this site and taking an online quiz. If you'd like to earn CPD hours by reading our content, you can apply for FPA membership today.

More about FPA membershipA consequence of the reduced super contribution caps from 1 July 2017 was an increased focus by financial advisers on non-super investment strategies, including investment in a client’s personal name. If managed well, utilising a client’s tax-free threshold may be an effective strategy, but the strategy can present some challenges too.

An inevitable consequence of the reduced super contribution caps from 1 July 2017 was an increased focus by financial advisers on non-super investment strategies, including investment in a client’s personal name.

If managed well, utilising a client’s tax-free threshold may be an effective strategy, but the strategy can present some challenges too.

The starting point is to understand the current personal income tax rules, and opportunities they present to manage an investment portfolio tax-effectively. Projecting a personal investment strategy position over the medium to long-term acts as a basis for comparing other strategies. It is then prudent to overlay some assessment of the legislative risk associated with the current tax rules, and the impact on alternative strategies.

Often the tax-free threshold is stated as $18,200, the threshold from which the 19 per cent marginal tax rate applies. In practice, however, a resident individual’s tax-free threshold is greater than $18,200 due to the effect of certain tax offsets – how much greater depends on age and marital status.

All resident individuals are entitled to the low income tax offset (LITO), subject to their level of taxable income. The maximum LITO is $445, which applies until taxable income exceeds $37,000, after which the entitlement reduces by 1.5 cents for each additional $1 of taxable income (or 1.5 per cent).

Seniors and pensioners who meet certain eligibility criteria are entitled to the seniors and pensioners tax offset (SAPTO). The maximum SAPTO is $2,230 for singles, reducing by 12.5 cents per $1 of income above $32,279. For each member of a couple, the maximum SAPTO is $1,602, reducing by 12.5 cents per $1 of income above $28,974.

The combination of these tax offsets results in the tax-free thresholds shown in Table 1. These thresholds mean there is considerable capacity to generate income from an investment portfolio in personal or joint names.

Based on our standard return assumptions (see Appendix), the long-term after-fees pre-tax projection rate for a balanced portfolio is 6.7 per cent per annum. The taxable income each year (including an allowance for capital gains tax on asset turnover) is approximately 4.8 per cent.

Table 1: Tax-free threshold

| Age | Marital status | Tax-free threshold** |

| To 65 years | N/A | $20,542 |

| 65+ years | Single | $32,279 |

| Married (per person)* | $28,974 |

A balance portfolio of approximately $430,000 would, based on the return assumptions used here, produce taxable income of just less than $20,542 in the first year; the tax-free threshold for an individual under age 65.

Likewise, for a married individual age 65 or more, a balanced portfolio in joint names of $1.21 million would produce taxable income for each spouse of just less than the tax-free threshold of $28,974. For a single senior individual, a portfolio of $675,000 would produce taxable income just less than the tax-free threshold of $32,279.

Keeping the level of taxable income to within these thresholds is a challenge. Growth in the portfolio will increase the level of taxable income generated in years subsequent to the first year. The effective tax rate on taxable income in excess of the tax-free threshold can be unexpectedly high, and a disincentive to personal investment.

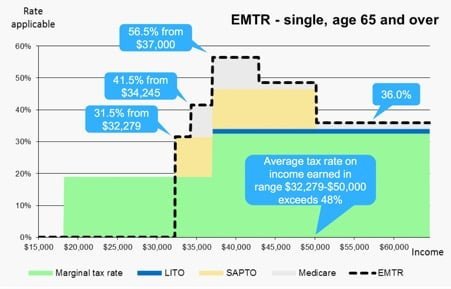

Consider again the position of a single individual over age 65. As noted above, their tax-free threshold is $32,279, but the next dollar of taxable income in excess of $32,279 is effectively taxed at 31.5 per cent, comprised of the marginal tax rate of 19 per cent plus loss of SAPTO at 12.5 cents per $1 of taxable income in excess of this threshold.

When taxable income reaches $37,000, the effective marginal tax rate peaks at a staggering 56.5 per cent, comprising of the 32.5 per cent marginal tax rate, LITO phase out at 1.5 per cent, SAPTO phase out at 12.5 per cent and Medicare levy phase in at 10 per cent.

Chart 1 shows the effective marginal tax rates (EMTR) at different levels of taxable income for a single senior individual.

Chart 1: Effective marginal tax rates for a single senior individual

Notes:

The effective marginal tax rate (EMTR) represents the amount forgone on an additional $1.00 of income at the income level stated on the x-axis. For example, if income equals $35,000, an additional $1 of income will result in $0.585 after the impact of tax and Medicare. Therefore the EMTR is 41.5%.

2017/18 marginal tax rates and tax offset rates and 2016/17 Medicare rates have been used in this analysis.

The amount of tax paid on income in the range from $32,279 to $50,000 is $8,532, which equates to an average tax rate in excess of 48 per cent. This exceeds the top marginal tax rate plus Medicare levy (47 per cent) that applies to taxable income in excess of $180,000.

Strategic planning of taxable income with regard to these high effective marginal tax rates is a potential value-add service for advisers.

Ideally, an individual would contribute funds into the accumulation phase of superannuation, where earnings are subject to a maximum tax rate of 15 per cent. But as noted above, the capacity to make super contributions has been significantly restricted by the 2017 super reform measures, so it’s assumed there is no opportunity to contribute large amounts to super.

Holding investment assets in a discretionary family trust, instead of in personal name, allows control of the level of income a range of individual beneficiaries receive each year. Targeting the tax-free threshold of each individual beneficiary may be effective, with any remaining trust income distributed to a corporate beneficiary.

Alternatively, investment bonds may be considered. Our analysis indicates that the net return generated by holding an investment bond over 10 years (assuming the returns on the balanced portfolio shown in the Appendix) is 4.8 per cent per annum, which compares favourably to holding the same portfolio in personal name at a marginal tax rate of 47 per cent (including Medicare levy), where the net return is 4.5 per cent per annum.

It is not appropriate to directly compare the 30 per cent tax rate that applies to investment returns generated within an investment bond with personal marginal tax rates. Capital gains realised within an investment bond do not attract any CGT discount, whereas capital gains realised by an individual may be 50 per cent exempt from tax. Based on the return assumptions detailed in the Appendix, the 30 per cent tax rate (with no CGT discounts), which applies to investment bonds, is equivalent to a personal marginal tax rate (with the 50 per cent CGT discount applying) of 40.5 per cent.

It follows that an investment bond will not be attractive compared to investment in personal name at marginal tax rates of less than 40.5 per cent (including Medicare).

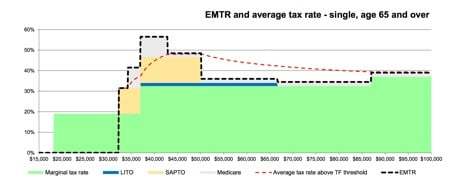

Chart 2 shows that for a single senior individual, the effective marginal tax rate exceeds 40.5 per cent for all income in the range $34,245 to $50,000. It also shows that the average tax rate on income in excess of the tax-free threshold exceeds 40.5 per cent when total taxable income is in the range $38,000 to $76,000.

Chart 2: Effective marginal tax rates and average tax rate

Rather than investing in personal name, these results indicate clients may be better off with some funds in personal name using their tax-free threshold, and some funds invested in an investment bond.

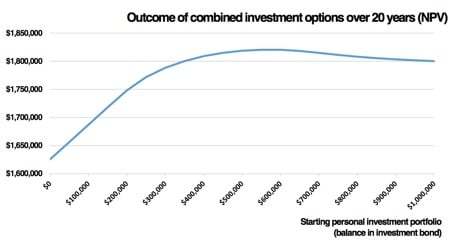

Chart 3 shows the outcomes of $1 million invested into various combinations of personal investment and investment bonds, ranging from 100 per cent in the investment bond (left hand side) to 100 per cent in personal name (right hand side), with $100,000 increments in between.

The chart shows that the optimum mix for a single senior individual (based on the return assumptions in the Appendix) is approximately $550,000 invested in personal name and $450,000 in an investment bond.

Chart 3: Combinations of personal investment and investment bonds

The Government has proposed legislation to progressively reduce the corporate tax rate for all corporate entities to 25 per cent by 1 July 2026. If the legislative amendments are passed by Parliament, the relative attraction of investment bonds will increase, assuming marginal tax rates and thresholds and personal tax offsets remain at current levels.

On 30 July 2017, Labor announced its proposal to tax distributions from discretionary trusts. The proposal was explained as an extension of the measures implemented in the early 1990s to tax unearned income of minors. The proposal would result in certain trust distributions paid to beneficiaries over 18 years of age being subject to a minimum tax rate of 30 per cent.

If implemented, this measure would impact significantly on the effectiveness of discretionary family trusts, potentially resulting in a shift of investment assets out of discretionary trusts and the wind-up of some trusts.

The Grattan Institute’s November 2016 paper, Age of entitlement: Age-based tax breaks, recommended reducing SAPTO to a maximum of $1,160 for singles (phasing out at 12.5 cents per dollar when income exceeds $27,000) and $390 for each member of a couple (phasing out when combined income exceeds $42,000). In addition, the paper recommends reducing the Medicare levy phase-in to $27,000 for senior singles and $42,000 combined for couples.

The combined effect of these recommendations would be an effective marginal tax rate for a single senior of 41.5 per cent applying in the range from $27,000 to $33,750. This would result in only marginal benefits in the effectiveness of investment bonds over personal investment above the $27,000 threshold.

The after-fees pre-tax projection rate of 6.7 per cent per annum used in this article is based on the asset class weightings, long-term income and capital growth projection rates and other assumptions in Table 2.

These rates aren’t guaranteed. They are provided as an illustration only and may vary from actual results. The projection rates aren’t intended to be (and shouldn’t be) relied on when making a decision about a particular financial product. Before making any financial decisions, you should seek personal financial advice from an Australian Financial Service licensee.

Table 2: Projection rate assumptions

| Asset Allocation | Capital Growth | Income | Franking Percentage | Tax free proportion | Tax deferred proportion | |

| Australian Equities | 30% | 5.0% | 3.5% | 60.0% | ||

| Property | 10% | 2.0% | 7.0% | 0.0% | 20.0% | |

| Cash | 5% | 4.5% | ||||

| Australian Fixed Interest | 20% | 6.5% | ||||

| Overseas Equities | 25% | 7.0% | 2.5% | |||

| Overseas Fixed Interest | 10% | 6.0% | ||||

| 100% | 3.5% | 4.5% | 21.0% | 0.0% | 3.1% | |

| Fees per annum | 1.5% | |||||

| Holding Period in years | 5.0 | Turnover p.a. | 20% |

To answer these questions for your 0.5 CPD hours, go to fpa.com.au/cpdmonthly